Funding Rate Revenue

Operators configure the base interest component on perpetuals that contributes directly to platform revenue on every funding interval.

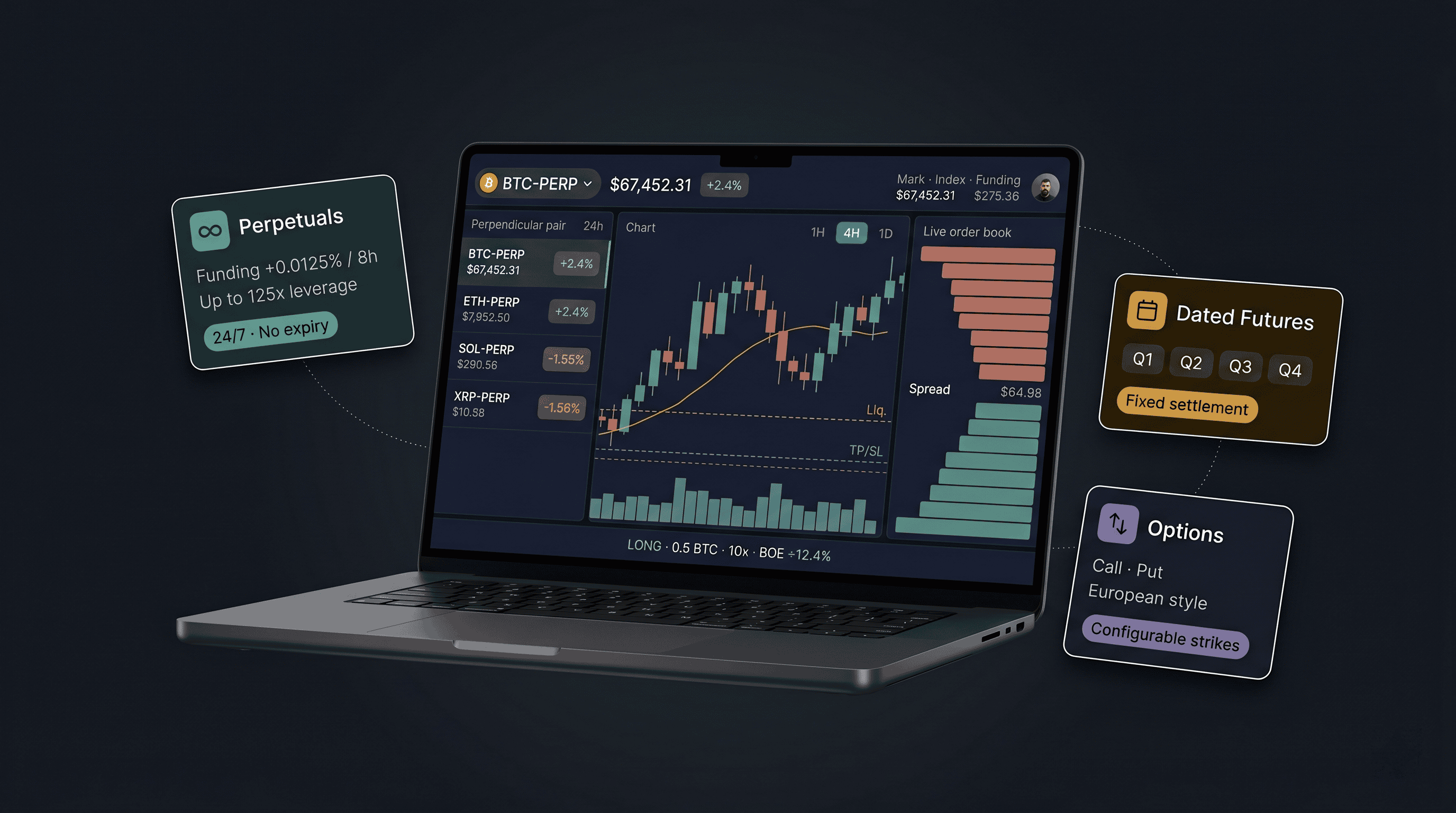

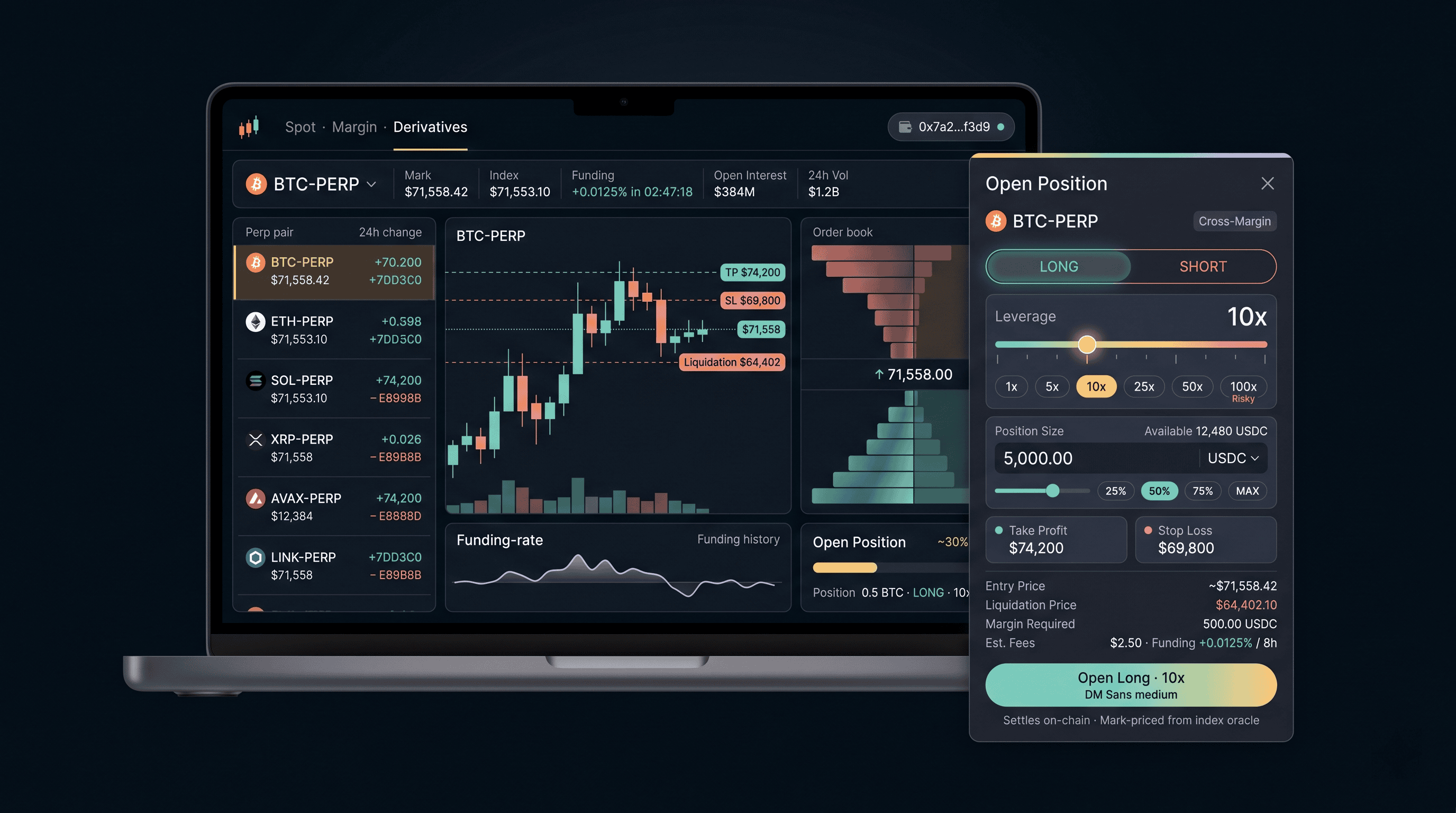

The Highest-Volume Segment in Crypto. Perpetual contracts, dated futures, and options on a single matching engine. Configurable leverage up to 125x. A unified risk engine with integrated clearing house mechanics, multi-source oracle pricing, insurance-fund-backed default management, and transparent ADL mechanics. Deep liquidity from the first contract traded.

Get StartedDeploy the full spectrum of derivative products from a single matching core.

No expiry. Funding settles on configurable intervals - anchoring contract price to spot via premium/discount mechanisms with operator-defined rate caps.

Aggregated venue depth extends to every derivative market with delta-neutral automated market making.

Optimizes execution across all connected sources simultaneously.

Large orders fragment across venues to minimize market impact.

Custom instruments launch with active order books from AMM bots.

Derivatives markets consistently outpace spot across all market conditions. Running a derivatives venue captures the highest-volume segment of the market.

Operators configure the base interest component on perpetuals that contributes directly to platform revenue on every funding interval.

Maker/taker fees on every contract executed. Higher notional values per trade relative to spot generate more absolute revenue per fill.

Execution spread on liquidated positions routes first to the insurance fund. Operator configures contribution tiers and retention logic.

Projects launching custom derivative instruments pay listing fees for inclusion in the derivatives environment.

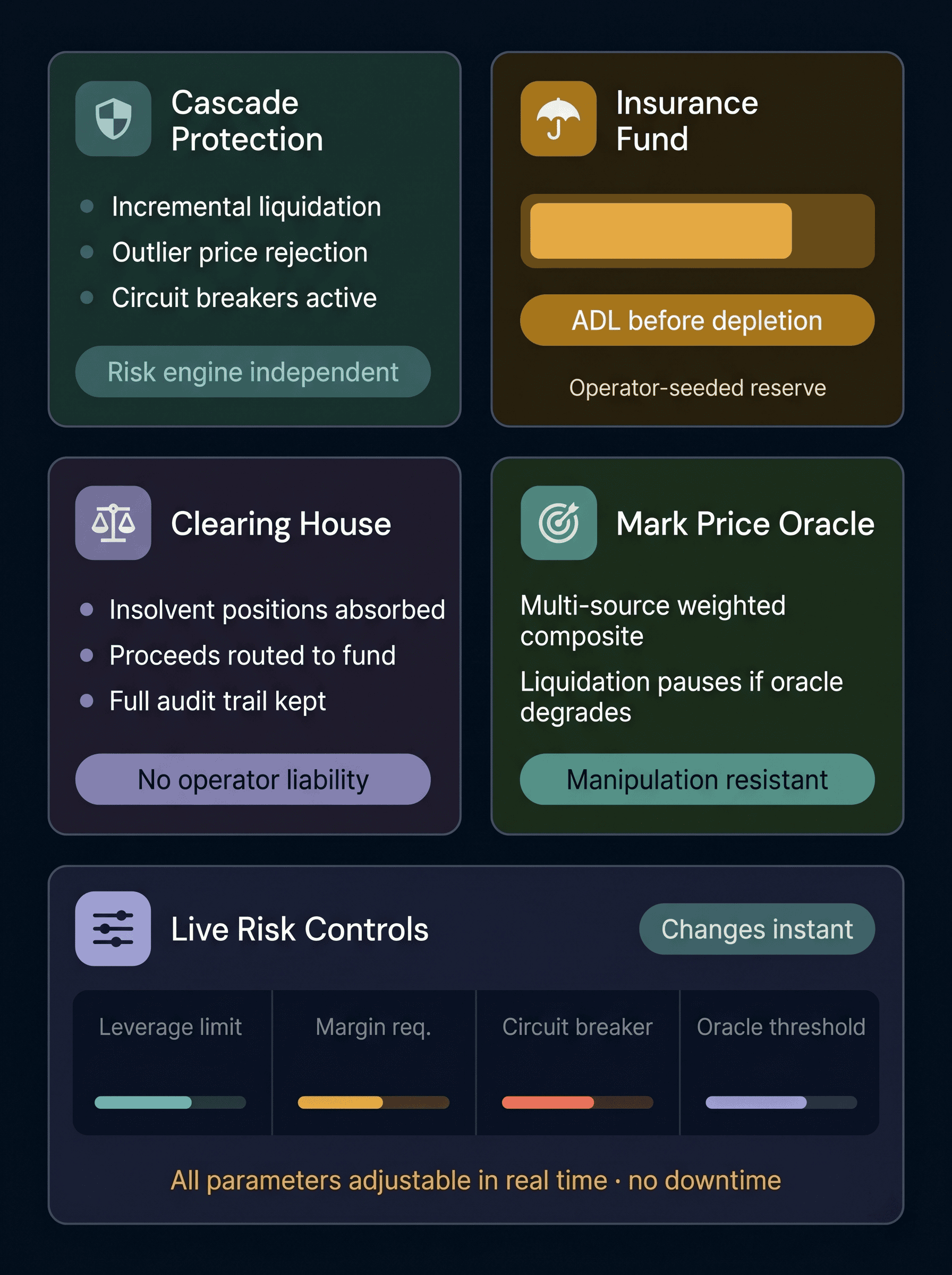

The risk engine operates as an independent subsystem — separate from the matching engine, with its own compute path and data feed. Position exposure, margin adequacy, and mark price evaluated on every tick across every open contract.

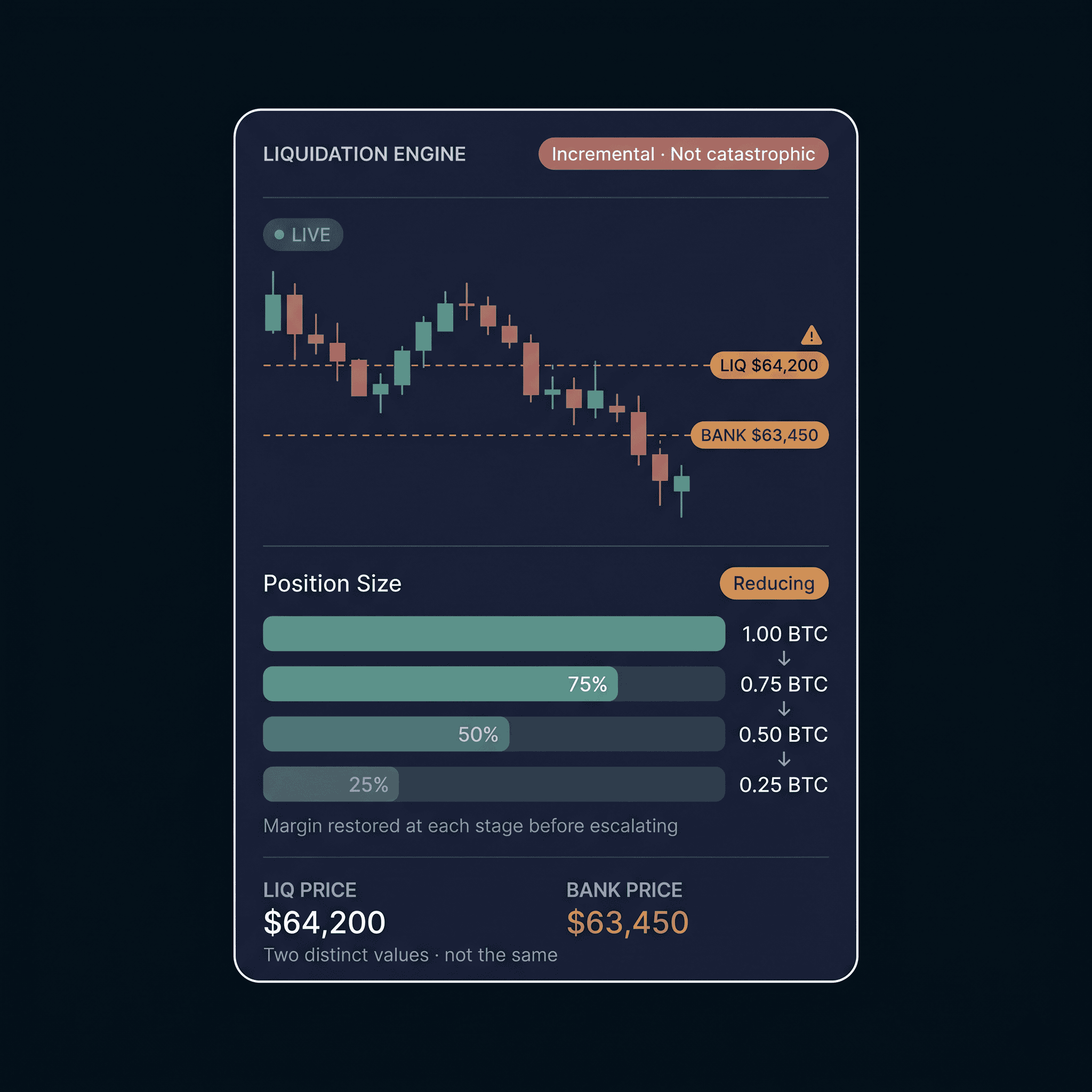

Liquidations trigger on mark price, not last traded price. A single manipulated print on a thin book cannot cascade an entire leverage stack.

Clearing Mechanics Embedded at the Engine Level. Clearing mechanics are embedded at the engine level — every contract traded carries structural guarantees, position management authorities, and default containment that define an institutional-grade derivatives venue.

When a position is liquidated, the engine closes at a price reflecting the liquidation execution cost. The residual between what the position's margin covers and what the engine recovers represents the clearing layer's operational spread. Proceeds route first to the insurance fund. The operator configures contribution tiers and retention logic from the admin panel.

When a position breaches bankruptcy price, the clearing layer takes over as counterparty. The original position holder's margin is exhausted; the clearing house absorbs the position and manages the close against the order book. For the enterprise operator: insolvent positions are handled systematically and deterministically. No manual intervention, no discretionary close-out, no user-facing loss mutualization.

Account balance shared across positions. Unrealized profit offsets margin consumption elsewhere. Maximum capital efficiency — a severe loss on one position draws from the full account.

Margin allocated per position. Loss capped to assigned margin. Account protected from cascading liquidation.

Margin posted in stablecoins, major tokens, or fiat. Real-time oracle valuation with configurable haircuts per asset. No forced conversion at position entry.

Define your own products; the engine handles the institutional mechanics.

Settlement Currency

USDT, USDC, other stablecoins, native tokens, or fiat-denominated settlement.

Settlement Method

Cash settlement against index, physical delivery of tokenized assets, or hybrid settlement logic.

Underlying

Any price feed the oracle layer can source — crypto assets, tokenized commodities, RWA indices, custom reference rates, sector indices, or proprietary benchmarks.

Expiry Structure

Fixed schedules, rolling windows, event-triggered expiry, or perpetual (no-expiry).

Contract Multiplier

Lot size and contract value denominated in operator-defined units.

Margin Model

Standard isolated or cross-margin; portfolio margining for multi-leg products.

Oracle Source

First-party data feeds, third-party price oracles, custom weighted composites, or operator-supplied reference prices.

Leverage Range

Minimum and maximum leverage caps per instrument.

Five-step protocol from definition to live deployment without downtime.

Configure underlying, settlement currency, expiry structure, margin model, leverage range, and contract multiplier in the admin panel.

Select or connect the price feed. Set source weighting, deviation thresholds, and fallback behavior.

Define position limits, maintenance margin requirements, insurance fund contribution rules, and circuit breaker thresholds.

Assign AMM bots with instrument-specific spread logic and depth tiers. Connect external hedging sources if available.

The contract goes live without platform downtime. Full risk engine, clearing house protections, and settlement infrastructure apply from the first trade.

100+ perpetual and futures pairs spanning the full crypto universe.

Advanced lifecycle tools for every trading stage.

Rate calculated from the premium/discount between mark price and spot index, combined with a base interest component. Maximum rate caps prevent extreme cost spikes. Historical funding accessible via API.

Dated contracts settle against a time-averaged index window — typically a 30-minute TWAP on the settlement venue index. The averaging window prevents last-second manipulation. Settlement price locks, positions settle, and finality is reached in the same tick.

European-style. Automatic exercise at expiry for in-the-money contracts against the settlement price. Premium and settlement flows execute within the same window.

Complete control over every risk and mechanical parameter.

| 1 | Leverage Limits | Per instrument, per user tier. Real-time adjustment. |

| 2 | Contract Specs | Tick size, lot size, multiplier, settlement type. |

| 3 | Margin Requirements | Initial, maintenance, and liquidation thresholds. |

| 4 | Funding Parameters | Interval, cap/floor, calculation method. |

| 5 | Oracle Config | Source selection, weighting, and fallback rules. |

| 6 | Insurance Fund | Contribution rules and depletion triggers. |

| 7 | ADL Rules | Activation triggers and ranking logic. |

| 8 | Position Limits | Per-user and aggregate market exposure caps. |

| 9 | Options Config | Strikes, expiries, premium model, and margin. |

| 10 | Circuit Breakers | Auto-halt on abnormal price movement or cascades. |

| 11 | Clearing Config | Liquidation fee routing and takeover thresholds. |

| 12 | Custom Contracts | Deploy new instruments and custom settlement logic. |

Need the highest-volume market segment. Derivatives consistently account for the majority of global crypto trading volume.

Need mission-critical risk infrastructure. Mark price oracles, multi-collateral margin, ADL with live priority indicators, and a complete clearing house audit trail.

Need derivative products on non-crypto underlyings. Configurable primitives support derivatives on oil, gas, metals, real estate indices, and treasury yield curves.

Need derivatives infrastructure without building a risk engine. The entire stack — oracle, liquidation, insurance fund, ADL, clearing house — ships pre-built.

Mark price is a multi-source weighted composite with outlier rejection and deviation circuit breakers. When oracle confidence degrades, liquidation processing pauses.

Liquidation price is where the engine begins closing a position. Bankruptcy price is where remaining margin reaches zero — closures past bankruptcy enter the default waterfall.

The insurance fund absorbs the shortfall first. If insufficient, ADL reduces ranked opposing positions. The shortfall is never socialized to users.

Yes. Configurable contract primitives support custom underlyings, settlement currencies, oracle sources, and expiry structures — deployed from the admin panel without downtime.

The clearing layer handles counterparty default, position takeover at bankruptcy, and the full default waterfall automatically. Complete audit trail, no manual intervention.

Walk through the full derivatives infrastructure — risk engine, clearing house mechanics, default waterfall, oracle architecture, custom contract configuration, and liquidity integration.

Book a Demo